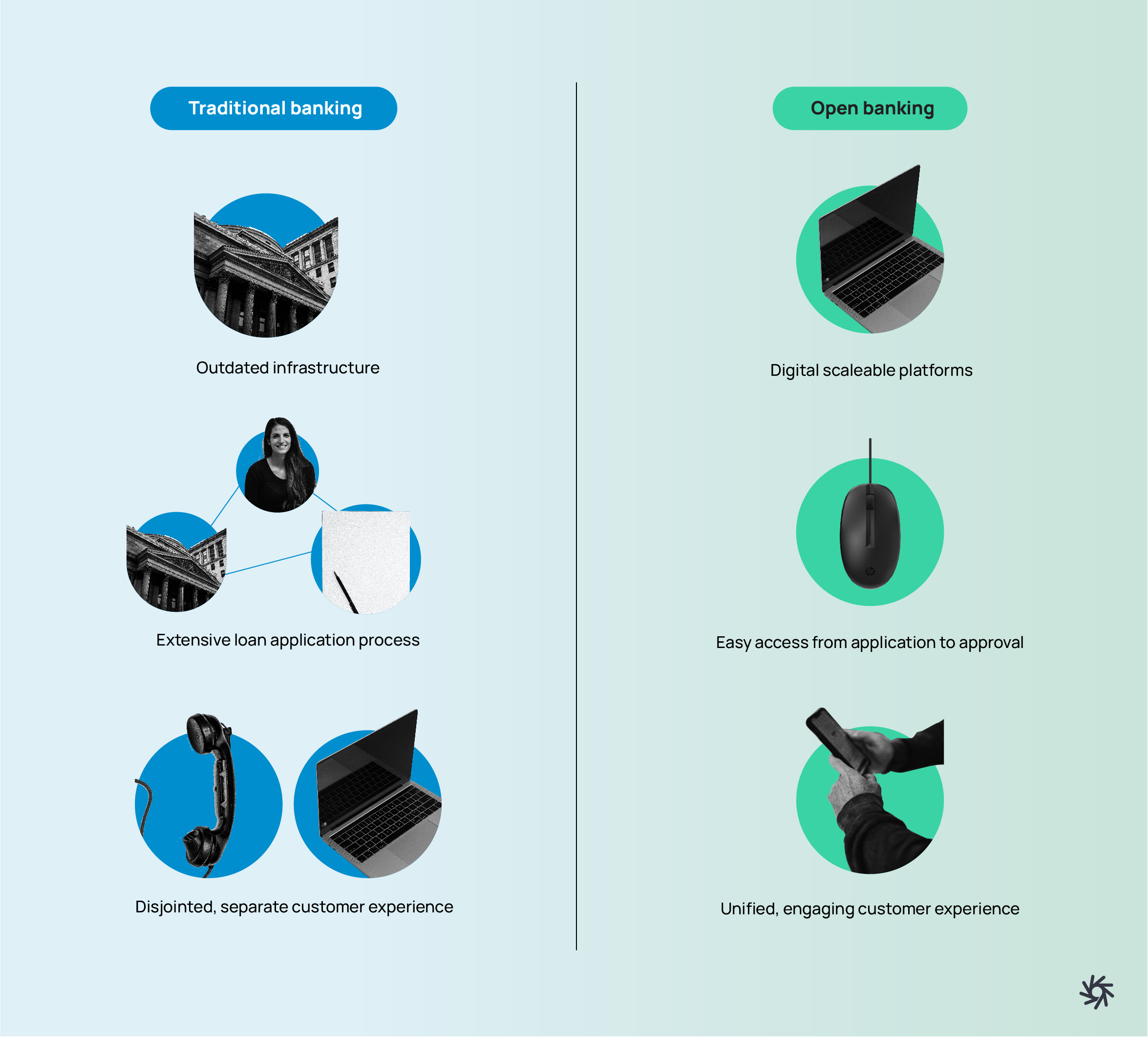

The value that open banking and open finance can bring to banking and financial services are clear: cheaper, better, faster, and more tailored solution sets for a diversifying customer base. What is sometimes unclear are the market dynamics that allow for consumers and businesses to be the beneficiary of innovation in this industry. Who are the key participants and what role do they plan in relationship to each other?

Open banking participants

There are five key groups that enable open banking to manifest in the way it does today. The following groups would also be similar in make-up to those than enable open finance, and in future, open data:

- Financial institutions – stewards of consumer and business data

- Third-party providers – integrates into a financial institution's APIs

- Fintechs – leverage TPP services to offer innovative solutions

- End-users – everyday consumers and businesses that use open banking services

- Regulator – stewards of this ecosystem to ensure its self-sufficiency

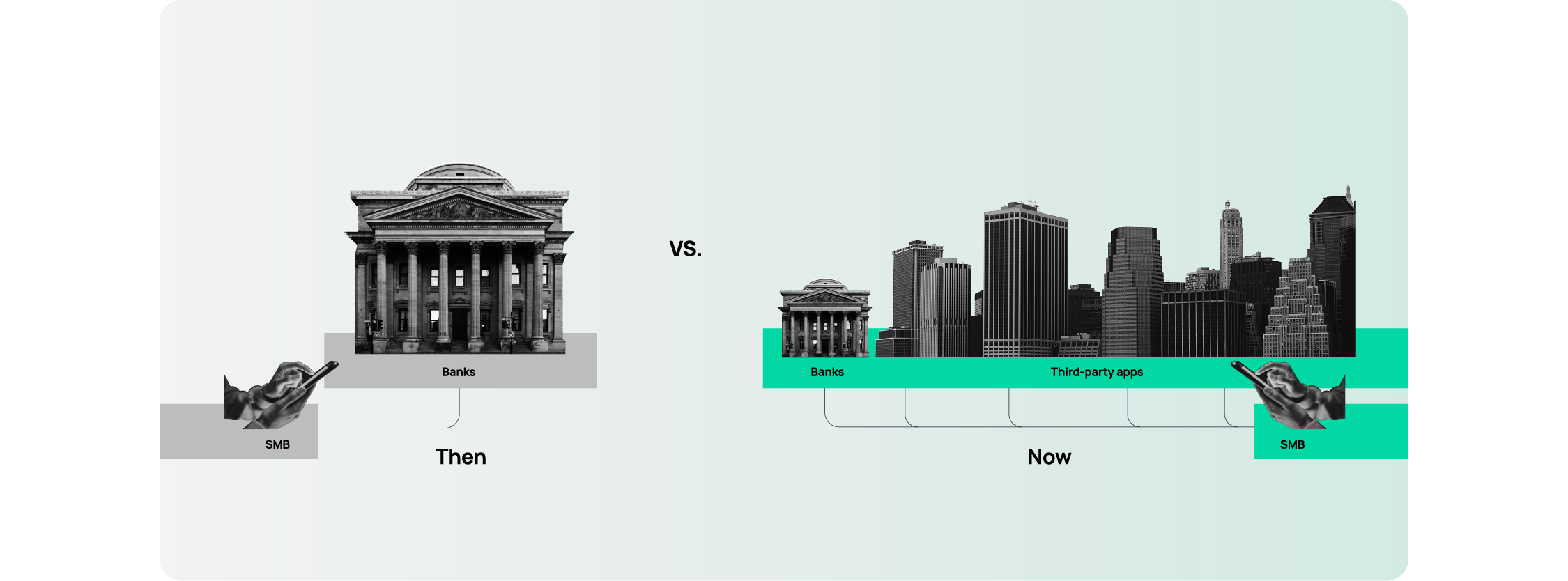

Financial institutions are, and have been, the de-facto storehouse for consumers and businesses banking and financial data since the inception of the commerce. As open banking proliferates and matures, their role would shift towards being the stewards of financial data compared to a hub for financial services. As such, each have an API that third-party providers can connect with to unlock the promise of open banking.

Third-party providers (TPP) are those in the market that work on the interoperability problem facing all open banking, and by extension, open data solutions. Often this role is played by the institutions that hold the large data stores, but increasingly it is disruptive private organizations — like Plaid, MX, and Salt Edge — who are among the world’s pre-eminent financial data aggregators. The role of the TPP is to provide the foundational infrastructure that enables the innovation promises of open banking.

Fintechs or financial technology companies are the group that turn the data, information, and knowledge made available by TPPs into innovative solutions for end users. The core competency for this group revolves around being able to build customer-centric financial service solutions — new digital experiences that often disrupt what traditional financial institutions offer. An authoritative example is Venmo, the mobile payment service in the USA. Without a financial data aggregator (TPP) like Plaid handling the technical infrastructure requirements, Venmo’s vision would be near impossible to realize.

End users are the beneficiaries of this ecosystem. The result of new market conditions that incentivize innovation and technology advancements, and a shift in attitudes sparked by the 2008 global financial crisis.

Regulators play the role of steward in this open banking ecosystem – their primary role is to tune the policy levers in such a way that will maximize the benefit and value to consumers and businesses. In other words, they are helping to redistribute market power away from financial institutions and back towards the customer. Policy moves can be roughly categorized into two buckets: opening access to financial data stores and ensuring that privacy controls remain top-of-mind during implementation.

Open banking ecosystem

The open banking ecosystem can be thought of circular. End users, consumers, and businesses transact and solicit financial services from financial institutions. Financial data is produced as a by-product of that interaction and is generally stored by the FI.

As financial data stores grow larger, third-party providers engage with financial institutions and work on connectivity between their platform and the bank’s API. This enables permissioned visibility into these datasets.

Fintech companies engage TPPs to build their digital solutions. Whether it’s a money management tool for families or a small business cash flow management product, the delivery requires connection to an end user’s financial data — which can be permissioned to any service (in theory).

These fintech companies then offer their products and services to the market. Whether they operate a B2C, B2B, or B2B2X model, the value accrues to the same place: the end user. Common pain points those users experience in traditional banking services can be directly addressed by innovative open banking solutions.

As consumers engage and interact more with fintech solutions, changes and updates to their financial data can be activated — data which is stored with the financial institution. Thanks to TPP services, end users can “write back” to the source as and when is appropriate. As an example, buying shares on Robinhood is enabled via payment from your bank account – an action in the Robinhood app translates back to an updated balance in the current account provided by your financial institution.

The position of regulators in this ecosystem is a little more detached. They set the policy direction and the baseline ground-rules that the groups outlined stick to. In summary, their goal is to widen and accelerate the flow of financial data that circulates from end user to financial institution to third-party provider — back to the fintech and the end user.