.png?width=4000&height=2250&name=UnbundlingVisual-InArticle-(v01).png)

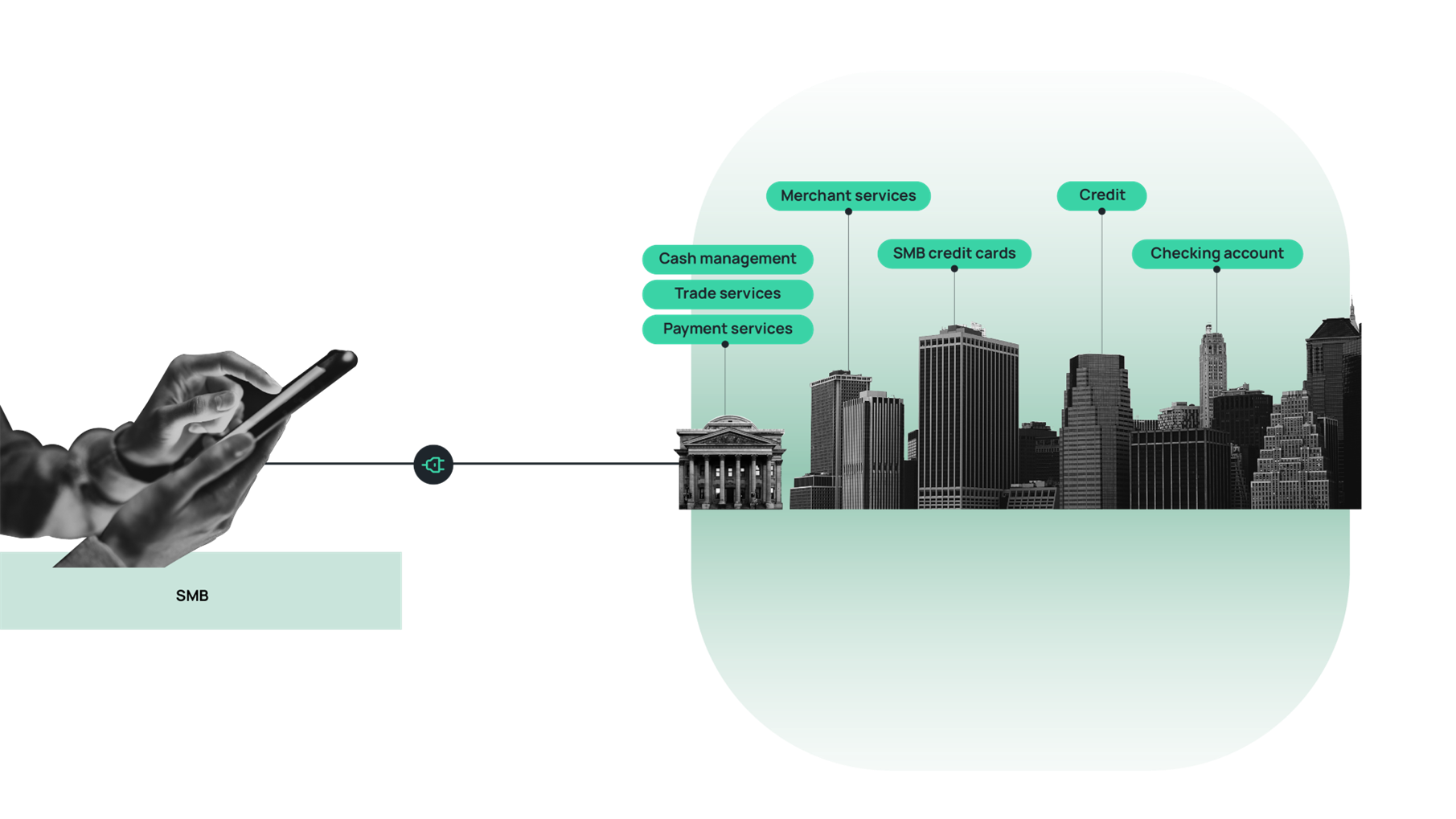

10 years ago, the bank was the center of a small businesses financial universe. Credit card, checking, savings, investments, payments, lending. You name it, and the bank was the first port-of-call for businesses to acquire financial services.

The sector, however, has since experienced, and continues to experience a great unbundling of core financial products and services eroding the market power of incumbents. No one provider is at the center of a small businesses' financial universe, instead, there are many providers that orbit around and have an influence in how they engage in their financial management practice.

These are now specialized suppliers of financial products and services that compete with incumbents. Some examples of opportunities an industry has formed around are: merchant services (eCommerce), lending, payments, digital banking, and more. While many of these propositions are competitive with the core banking offering, there are some like the dynamic with providers of general ledger services remains unchanged in that it is co-operative if not symbiotic.

What incumbent financial institutions need to be weary of are the few that breakthrough and out of their niches and begin encroaching on the core banking offering. Square is one such example, beginning with a payments solution for micro-businesses in the late 2000s to now offering the gamut of financial services including merchant services (point-of-sale, invoicing, payment processing, etc.), business checking and savings products, a suite of payroll solutions, and lending products to name a few. Stripe would be another example, as is Brex and Ramp, of these fintech-cum-financial institutions that are now in direct competition with incumbents and are eligible to become the center of their target customers' financial universe.

Financial institutions have a big opportunity to become the hub of small businesses' financial and operational activities, despite the intense competition in this space. This opportunity is becoming more apparent with the emergence of open banking and open technologies, which allow banks to integrate their customers' business and performance data and offer a more comprehensive banking experience. As a result, business owners can manage their finances through the bank while also accessing embedded tools that cover more aspects of their business management needs. The bank could become the go-to platform for managing a business's operations, making it a launchpad for business operators.

If successful, banks will deepen customer relationships, transform to become a trusted partner, and default to being the co-pilot for small business owners and operators to run their day-to-day.

Introducing 9Spokes. We unlock the potential of open data and open banking by collecting consented data from businesses to give financial institutions a powerful set of tools to engage their business customers. These tools make the financial institution "the center" of their business customers’ daily financial lives.